Global green ammonia market to reach $38.5bn by 2033, driven by large-scale projects

Green ammonia reaches a new industrial milestone with 428 active projects and over $11bn in investments, highlighting accelerated sector growth across Asia, the Middle East, Europe and the Americas.

| Sectors | Hydrogen Energy |

|---|---|

| Themes | Markets & Finance, Sector Analysis |

| Companies | Envision Energy, ACWA Power |

| Countries | Brazil, China, India, Saudi Arabia, United States |

The global green ammonia market is projected to reach a valuation of $38.5bn by 2033, up from $662mn in 2024, supported by a compound annual growth rate of 60.36%. This rapid progress is based on the launch of 428 low-emission projects recorded in August 2024, with a combined nameplate capacity of 372.5 million tonnes per year.

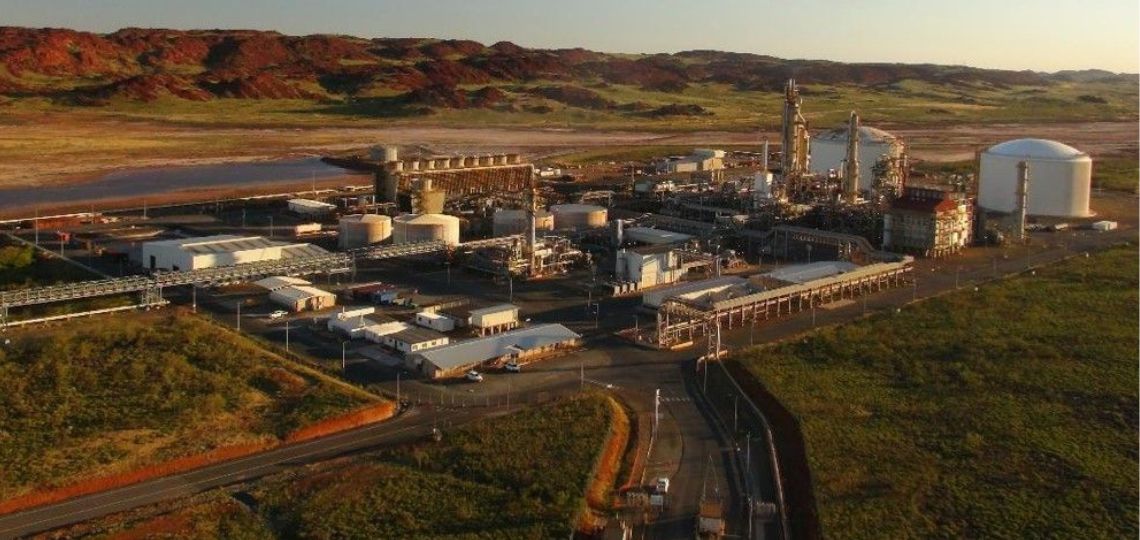

Major projects confirm industrial viability

Several large-scale facilities are expected to become operational between 2024 and 2025. In Saudi Arabia, a plant is targeting an operational capacity of 1.2 million tonnes by 2025. In India, AM Green Ammonia has reached a final investment decision for a facility with an annual output of 1 million tonnes, while ACWA Power is developing a 2.2 million-tonne complex in Yanbu. In China, Envision Energy is targeting 300,000 tonnes of commercial capacity by late 2025. In the United Arab Emirates, a 40,000-tonne facility complements a landscape dominated by multi-megaton initiatives.

Massive capital flows structure a growing sector

The acceleration of the project pipeline is being fuelled by substantial financial commitments. HNH Energy plans to invest $11bn in a Chilean project. India’s ACME Group has allocated $6bn to its production plans, while Hygenco is targeting $2.5bn over three years. In Europe, a programme backed by the European Union represents $11.9bn. In North America, two projects in the northern US are valued between $1.3bn and $2.2bn.

Long-term offtake agreements secure demand

Market maturation is accompanied by a growing number of long-term offtake contracts. In January 2024, ACME Group signed a 1.2 million tonnes per annum agreement with IHI Corporation. In August 2024, India concluded its first green ammonia export deal with Japan. In June 2025, Marubeni finalised a contract for supply from China, while Yara Clean Ammonia secured a term agreement in Egypt. In India, an August 2025 auction saw Jakson Green and ACME commit to 85,000 and 50,000 tonnes respectively under ten-year contracts.

Price competitiveness strengthens India’s positioning

Pricing dynamics are shifting towards improved competitiveness. In 2024, US Gulf Coast contracts ranged between $600 and $1,000 per tonne. In August 2025, ACME Cleantech Solutions secured a record-low price of $640/tonne in an Indian auction. Jakson Green followed with a price of $583/tonne. Average prices in Q2 2025 were $782/tonne in the US, $827/tonne in Germany, and $707/tonne in India, highlighting the region’s cost advantages.

Regulatory incentives accelerate market development

Government support is proving critical. India launched a ₹130.5bn ($1.57bn) subsidy programme in January 2024, offering tiered incentives over three years for green ammonia producers. In the United States, the Department of Energy supports one project with up to $1.6bn in loan guarantees. Morocco has reserved 1 million hectares of land for Power-to-X developments, including 300,000 hectares allocated by October 2025.

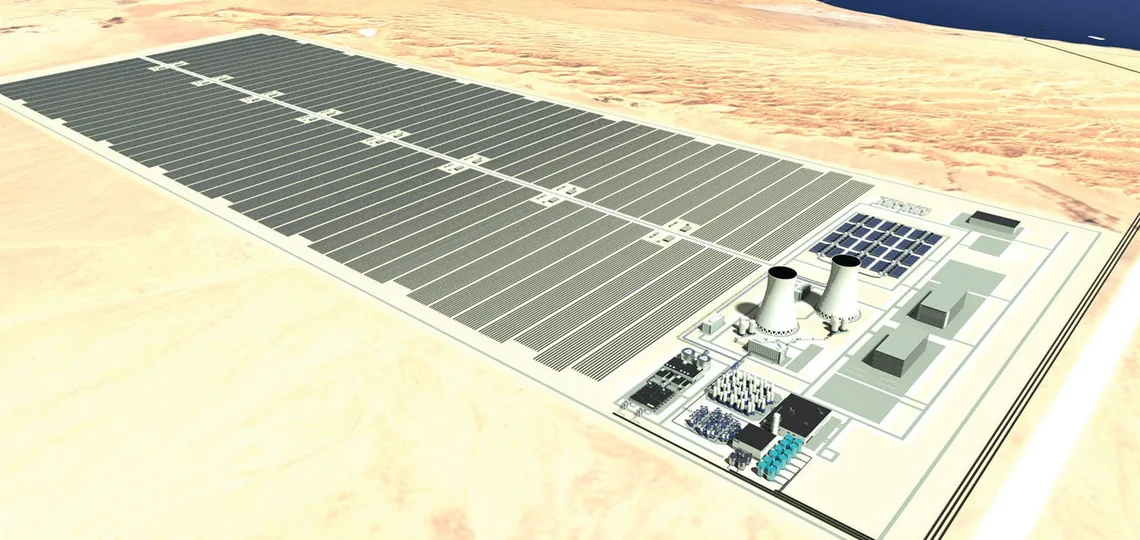

Electrolyser deployment confirms transition readiness

Technology availability aligns with industrial goals. The NEOM project will use 4 GW of renewable power. In India, an October 2024 tender targets 1,125 MW of green electricity. Topsoe plans to produce 500 MW annually of solid oxide electrolyser modules. AM Green will install 1.3 GW of capacity at Kakinada, and Hydrogen City in Texas will incorporate a 2.2 GW system.

Shipping and agriculture sectors drive demand

The maritime industry is positioning green ammonia as a zero-carbon fuel. Ohmium’s floating production project, announced in October 2024, is designed to produce 300,000 tonnes annually. Agriculture remains a steady demand base: Yara’s plant will produce 20,500 tonnes of renewable ammonia, converted into 60,000 to 80,000 tonnes of green fertiliser. TalusAg’s modular system in Iowa produces up to 20 tonnes per day.

Infrastructure planning integrates midstream logistics

Market success depends on logistics capacity. Hydrogen City includes an underground storage facility for 24,000 tonnes of hydrogen, connected to a 120-kilometre pipeline. Such midstream assets are critical to balance supply-demand fluctuations and enable large-scale trade.

Specialised developers lead global competition

Experienced developers dominate the global landscape. ACME Group, AM Green, Hygenco, Envision Energy, Yara International, ACWA Power and Helios Industry are leading high-capacity initiatives. Brazil’s H2Brazil is deploying a 700,000-tonne facility backed by a €1.3bn investment. In the US, First Ammonia is partnering with Topsoe on a 100,000-tonne facility scheduled for 2027.