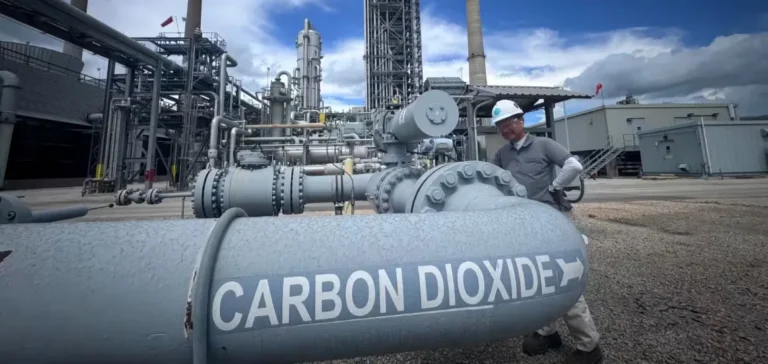

Japan aims to reach a carbon capture, utilisation and storage (CCUS) capacity of 12.5 million tonnes per annum (Mtpa) by 2035, up from just 0.3 Mtpa today. This growth, primarily driven by hard-to-abate industrial sectors, positions the country among Asia-Pacific’s leaders in the development of this technology.

International partnerships, a prerequisite for success

Around 60% of the targeted capacity depends on cross-border storage partnerships, particularly with countries such as Australia, Indonesia and Malaysia. Maritime CO2 transport from Japan to Australia is estimated to cost seven to nine times more than domestic transport. However, early movers could reduce this increase to 15–20% through strategic agreements and by securing favourable storage sites.

According to Wood Mackenzie, advanced carbon capture and storage projects shortlisted by the Japanese government represent over 20 Mtpa of potential capacity. Most of this capacity is still subject to negotiations, casting doubt on the country’s ability to meet its 2030 roadmap.

Strengthened policy framework to support projects

Japan currently ranks second in Asia-Pacific in terms of regulatory readiness for CCUS, behind only Australia. This is due to the clarity of its targets, the existence of a dedicated storage regulatory regime and improved access to low-cost public financing.

The introduction of a fuel levy and the conversion of the emissions trading scheme (GX ETS) from voluntary to mandatory have strengthened economic incentives for CCUS adoption across industrial sectors.

Investment needs remain significant

Wood Mackenzie estimates that at least USD 10 billion (JPY1.52tn) in government support will be required by 2050 to ensure the rollout of CCUS, based on a carbon price reaching USD 69 per tonne by mid-century. This support is essential, given the current profitability constraints of CCUS projects worldwide.

A study of 200 CCUS projects across multiple geographies indicates that revenues from current mechanisms such as emissions trading systems or low-carbon product premiums often fall short of covering project costs. Economic viability depends on stacking multiple forms of support: capital grants, operational subsidies, tax relief and other incentives.

Strategic positioning in the Asia-Pacific region

Japan could benefit from a first-mover advantage by securing bilateral agreements with countries offering large storage capacities. Several regional hubs are being developed to receive CO2 captured abroad, paving the way for a new carbon logistics network across Asia.

At the same time, Japan’s domestic focus on innovation, particularly in technologies like Direct Air Capture (DAC) and Bioenergy with Carbon Capture and Storage (BECCS), could strengthen its competitive position. Success will depend on the country’s ability to combine domestic innovation with targeted regional cooperation.