US crude falls below $55 per barrel, lowest level since 2021

Oil prices drop amid progress in Ukraine talks and expectations of oversupply, pushing West Texas Intermediate below $55 for the first time in nearly five years.

| Sector | Pétrole |

|---|---|

| Theme | Marchés & Finance, Prix |

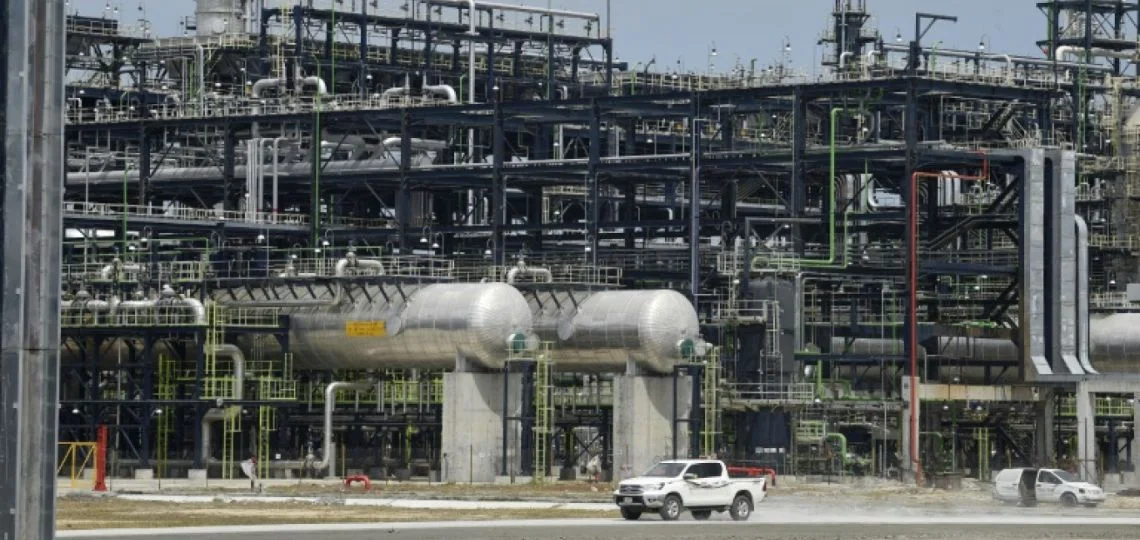

The price of US crude oil fell on Tuesday to a level not seen since February 2021, briefly slipping below the $55 mark. The barrel of West Texas Intermediate (WTI) for January delivery reached $54.98 during the session before slightly rebounding to $55.32, a 2.64% decline. This drop marks a significant shift for markets, faced with a combination of easing geopolitical tensions and oversupply expectations.

Comments

Sign in to leave a comment.